Before an insurer knows anything about you, your postcode or your no-claims history, it already has a starting point for what your cover might cost: the car itself. Every car on UK roads sits in a car insurance group, and that group is one of the first things a quote is built on. Understanding how the system works helps you read a quote with a clearer eye, and it can save you money at the point that matters most, which is when you are choosing which car to drive next.

Here is how car insurance groups work, who sets them, and what the new rating system arriving on the newest cars means for you.

What is a car insurance group?

A car insurance group is a rating that tells insurers, in broad terms, how expensive a particular make and model is likely to be to insure. Cars are sorted into 50 groups. A car in group 2 is among the cheapest to cover, and a car in group 50 sits at the most expensive end.

The group is set for a specific model, engine, and trim, not the badge on the bonnet. Two versions of the same car can sit several groups apart, because a larger engine, a higher list price or extra equipment changes the picture. It is a guide to relative cost rather than a price in itself. A low group does not promise a cheap premium, and a high group does not huarantee an expensive one, because plenty of other factors come into play once an insurer looks at you and how you drive.

Who decides car insurance groups?

The groups are produced by a body called the Group Rating Panel, which brings together members from the Association of British Insurers and the Lloyd’s Market Association. The research behind the ratings is carried out and administered by Thatcham Research, the motor insurers’ research centre. The panel meets every month to assess new models as they reach the market and place them in a group before they go on sale.

Thatcham does the engineering side of the work. It runs low-speed crash tests, strips cars down to see how repairable they are, times how long a typical repair takes and prices the parts involved. The insurer members bring the claims data. Together they arrive at a number that the wider market can use as a baseline.

That word, baseline, matters. Insurers are not bound to follow the group rating. They use it as a reference alongside their own claims experience, then price as they see fit. It is why the same car can return quotes that differ by a wide margin from one insurer to the next, and why comparing actual quotes always beats comparing groups alone.

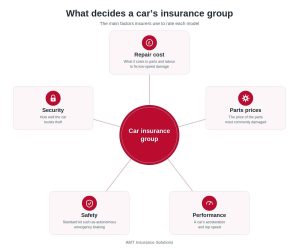

What puts a car in a particular group?

Several factors feed into a car’s group, and most of them come back to one question: if something goes wrong, how much will it cost to put right?

Repair cost is the single biggest input. Thatcham runs controlled low-speed impacts, close to the kind of knocks you might pick up in a car park, and works out what it costs in parts and labour to return the car to its previous condition. Parts prices feed in through a set basket of commonly damaged components, so that cars can be compared on a like-for-like basis. Repair times count too, because a model that takes longer in the body shop costs more to put right.

The car’s value when new is factored in, since that sets the cost of replacing it if it is written off. Performance plays a part, with the quoted 0 to 62mph time and top speed both considered, as quicker cars tend to be involved in costlier claims. Safety and security work in the other direction. Strong safety equipment, such as autonomous emergency braking fitted as standard, can move a car down a group, and good security can do the same.

What the letter after the group number means

You will often see a letter alongside the group number, such as 15E or 9D. That letter is Thatcham’s way of recording how a car’s security compares to what is expected for its type.

The letters break down as follows. E means the car exceeds the security standard for its type, so it has been moved down a group. A means an acceptable standard for its type. D means it does not meet the standard, so it has been moved up a group. U means an unacceptable standard, and an insurer may ask for aftermarket security to be fitted before agreeing to cover it. P means provisional, used when there is not enough data at launch to rate the car fully. G marks a grey import, a car not officially sold in the UK, which is assessed case by case.

In practice that means security can nudge a car either way. A car assessed at group 8 with strong security might end up rated 7E, while the same car with poor security could be rated 9D.

The new vehicle risk rating system

There is a change worth knowing about, because it affects the newest cars on the market. In September 2024, Thatcham introduced the Vehicle Risk Rating, or VRR, which applies to brand-new model ranges first sold in the UK from 1 August 2024.

Rather than a single number from 1 to 50, the VRR scores a car from 1 to 99 across five separate areas: performance, damageability, repairability, safety and security. The aim is to give insurers a more detailed read on modern cars, which carry far more electronics and driver-assistance technology than the older system was built to capture. These ratings began to be published from early 2025.

For most drivers, nothing changes day to day. If your car is not part of the brand-new model range launched from August 2024 onward, it keeps its familiar 1 to 50 group rating. Over time, as more new models come through under the VRR, you will see both systems referenced, so it is helpful to know which one applies to the car in front of you.

How insurance groups work across the range

You do not need a list of models to get a feel for the scale, because the pattern is fairly consistent.

At the lower end of the range sit small, modest cars: city cars and small hatchbacks with smaller engines, lower list prices and inexpensive, widely available parts. These are typically the cheapest to insure, which is why they are so often recommended as first cars.

Through the lower-middle of the range you find larger superminis and family hatchbacks, with a little more performance and equipment but still straightforward and affordable to repair. The middle of the range covers many mainstream family cars and crossovers, where size, value , and repair complexity start to climb. Towards the upper end come more powerful, more expensive and more complex cars, including many performance models and larger premium vehicles. At the very top sit the fastest, most valuable and most specialised cars, where high performance and costly repairs push them into the priciest groups.

The takeaway is simple enough: as a car gets faster, pricer or more complicated to fix, it tends to move up the scale.

Do electric cars sit in higher groups?

Often, yes, at least for now. Electric cars frequently land in higher groups than a similar sized petrol model, mainly because they currently cost more to repair and some parts are harder to source. Thatcham has noted that electric vehicles can be around 25% more expensive to repair, with repair times roughly 14% longer than equivalent petrol or diesel cars.

This varies a lot by model, and the gap is expected to narrow as the repair sector grows around electric vehicles. There is more to it than the group alone, so it is worth understanding the full picture of what shapes an electric car’s premium.

How to check your car’s insurance group

You can look up any car’s group on Thatcham Research’s website using its My Vehicle Search tool, where you enter the make, model, and a few details to find the rating. Most comparison sites also display the group on the quote screen once you run a search, so you can see it next to the actual price being offered.

If you are weighing up two cars, checking the group for the exact version you have in mind, the right engine and trim, gives you a fairer comparison than looking at the model in general.

Does a car’s insurance group ever change?

The group assigned to a model is fixed. It does not automatically drop as the car gets older. What can change is how an insurer prices it, because as a car ages and its value falls, and its parts become more common, some insurers may quote more favourably even though the group itself has not moved.

Modifications are a separate matter. They do not change a car’s official group, but they can affect what you pay, and they need to be declared. anything fitted that was not there when the car left the factory, from alloy wheels to performance or styling changes, should be mentioned to your insurer, as it can alter how the risk is viewed.

What else affects your premium?

The group sets a baseline, but a good deal fo your premium comes down to factors that have nothing to do with the car. Insurers look at your age and driving experience, where you live and where the car is kept overnight, your claims and convictions history, your annual mileage, your occupation and the level of cover you choose. Choices such as a higher voluntary excess or a no-claims discount built up over time also feed into the final figure.

Some of these you cannot change, but several you can influence, and small adjustments can add up. One option some drivers consider, particularly newer rivers facing higher premiums, is a telematics policy, where a device records how the car is driven and rewards careful driving at renewal.

Using insurance groups when choosing your next car

The most useful moment to think about insurance groups is before you commit to a car, not after. Two cars that look similar on the forecourt, and cost much the same to buy, can sit several groups apart and carry noticeably different running costs over the years you keep them. Factoring the group in early, alongside fuel, tax and servicing, gives you a truer sense of what a car will cost to live with.

It is one piece of the puzzle rather than the whole of it, so the sensible final step is always to run a real quote on the specific car and your own details before you decide.

We arrange a wide range of motor insurance for people and businesses alike. Get in touch with us to discuss your requirements.